How Much Is Gap Insurance? A Comprehensive Guide to Protecting Your Investment

You’ve just signed the papers for a brand-new car. The smell of fresh leather is intoxicating, the dashboard is glowing with high-tech displays, and for a moment, everything feels perfect. But as you drive off the lot, a harsh reality settles in: your car just lost thousands of dollars in value the second the tires hit the public pavement.

In the insurance world, this is known as the “gap.” If you were to total that car on the way home, your standard auto insurance would likely only pay you what the car is worth now (its Actual Cash Value), not what you paid for it or what you still owe the bank. This financial crater can leave you owing $5,000, $10,000, or even more for a car that no longer exists.

This is where Gap Insurance (Guaranteed Asset Protection) comes in. But the burning question for every savvy consumer is: How much does gap insurance actually cost?

In this exhaustive guide, we will break down every penny, every factor, and every strategy to ensure you aren’t overpaying while protecting your financial future.

1. What Exactly Is Gap Insurance? (The Human Definition)

Before we talk about the “how much,” we need to understand the “what.” Gap insurance isn’t a luxury; for many, it’s a financial life jacket.

When you buy a car, especially with a low down payment or a long-term loan, you are often “underwater” or “upside down” on your loan. This means you owe the lender more than the car’s market value.

The Scenario:

- Loan Balance: $35,000

- Market Value (ACV): $28,000

- The “Gap”: $7,000

If your car is stolen or totaled, your primary insurer sends a check for $28,000. Without gap insurance, you are personally responsible for writing a $7,000 check to the bank for a car you can’t even drive anymore. Gap insurance covers that $7,000 difference.

2. The Average Cost of Gap Insurance in the US

The price of gap insurance varies wildly depending on where you buy it. In the United States, you generally have three main avenues for purchase:

A. Buying from a Dealership

This is the most common but also the most expensive route. Dealers often bake the cost into your monthly financing.

- Typical Cost: $400 to $1,000 (flat fee).

- The Trap: Because this is often financed, you are also paying interest on the gap insurance itself over 60 or 72 months. A $600 policy could end up costing you $900 by the time the loan is paid off.

B. Buying from Your Current Auto Insurer

Most major carriers (Progressive, State Farm, Allstate, etc.) offer gap insurance as an add-on (endorsement) to your existing comprehensive and collision policy.

- Typical Cost: $20 to $60 per year.

- The Benefit: This is significantly cheaper. It usually adds about 5% to 6% to your annual premium.

C. Standalone Specialized Providers

Some companies specialize only in gap coverage or mechanical breakdown insurance.

- Typical Cost: $200 to $300 (one-time fee).

3. Why Is There Such a Price Discrepancy?

You might wonder why a dealer charges $800 while an insurance company charges $40. The answer isn’t just “corporate greed”—though markups are real.

- Convenience Factor: Dealerships charge for the “point of sale” convenience. You’re already signing fifty papers; what’s one more?

- Profit Margins: Gap insurance is a high-margin product for dealerships. It is one of the primary ways Finance & Insurance (F&I) managers make their commissions.

- Risk Assessment: Insurance companies already have your data. They know your driving record and your credit score. They can price the risk more accurately and affordably than a dealership’s flat-rate pricing.

4. Key Factors That Influence Your Gap Insurance Rate

No two drivers will pay the exact same amount for gap insurance. Here are the variables that the “algorithms” look at when determining your price:

I. The Value of the Vehicle

A $100,000 Tesla Model S Plaid depreciates much faster in dollar terms than a $25,000 Honda Civic. The larger the potential “gap,” the higher the premium. Luxury vehicles and high-end SUVs typically command higher gap insurance rates.

II. Your Location (State Regulations)

Insurance is regulated at the state level in the US. Some states have caps on how much a dealer can charge for gap insurance. Other states, like New York or California, have specific consumer protection laws that influence availability and pricing.

III. Your Loan-to-Value (LTV) Ratio

If you put $0 down on a car, your LTV is high, and your risk to the insurer is massive. If you put 30% down, your gap is much smaller (or non-existent), leading to lower rates if you choose to buy coverage at all.

IV. Length of the Loan

A 72-month or 84-month loan means you will stay “underwater” for a much longer period. Short-term loans (36 months) reach equity faster, reducing the time the gap insurance is actually “at risk.”

5. Dealership vs. Private Insurance: A Detailed Comparison

Let’s dive deeper into the pros and cons of each to help you decide where to spend your money.

The Dealership Route

- Pros: Easy to set up; covers the entire loan regardless of your personal insurance carrier; often covers your primary insurance deductible (up to $500 or $1,000).

- Cons: Extremely expensive; subject to interest rates; harder to cancel for a full refund.

The Auto Insurance Carrier Route

- Pros: Dirt cheap; easy to cancel once you have positive equity; billed with your regular premium.

- Cons: Only works if you have comprehensive/collision coverage; may not cover your deductible; usually only available for the original owner of a new car.

6. Real-World Math: Is It Worth It?

Let’s look at a realistic five-year ownership cycle for a $40,000 SUV.

- Year 1: Car value drops to $32,000. Loan balance is $38,000. Gap = $6,000.

- Year 2: Car value drops to $27,000. Loan balance is $33,000. Gap = $6,000.

- Year 3: Car value drops to $23,000. Loan balance is $27,000. Gap = $4,000.

- Year 4: Car value drops to $19,000. Loan balance is $20,000. Gap = $1,000.

- Year 5: Car value drops to $16,000. Loan balance is $13,000. Equity = $3,000.

In this scenario, you need gap insurance for about 4 years.

- Dealer Cost: $800 upfront + interest.

- Insurance Carrier Cost: $40/year x 4 years = $160 total.

The choice is clear for those looking to save money.

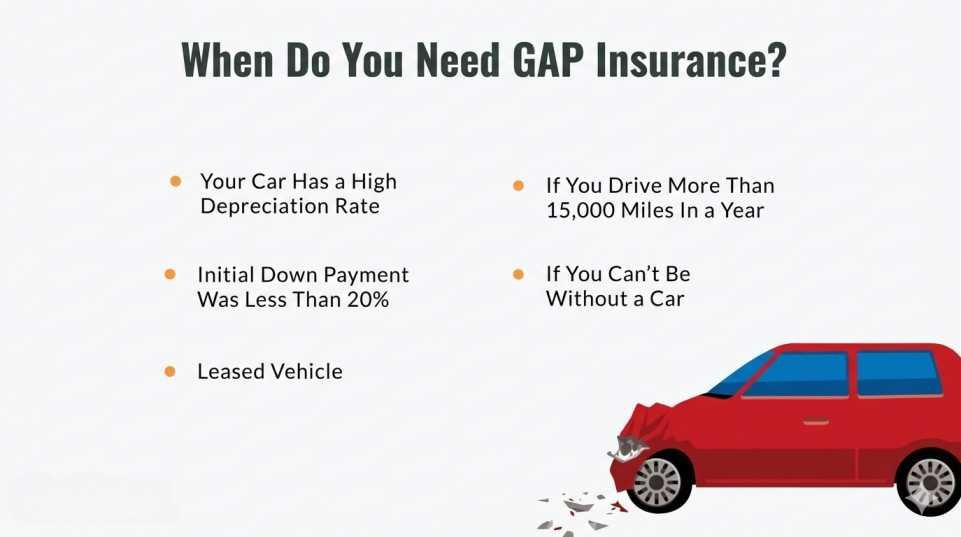

7. Who Should ABSOLUTELY Buy Gap Insurance?

Not everyone needs this coverage. If you paid cash for your car, gap insurance is a waste of money because you own the asset outright. However, you should strongly consider it if:

- You made a small down payment: Less than 20% down almost guarantees you’ll be underwater for a while.

- You financed for 60 months or more: Long loans are the primary driver of negative equity.

- You drive a lot of miles: Higher mileage causes faster depreciation.

- You rolled negative equity from a previous loan: If you owed $3,000 on your old car and added it to the new loan, you are starting $3,000 behind the curve.

- You leased the car: Most lease agreements actually require gap insurance (and many include it for free—check your contract!).

8. State-Specific Insights (USA)

The cost of gap insurance can vary by your zip code.

- Texas & Florida: These states have high rates of total losses due to floods and hurricanes. While gap insurance premiums don’t fluctuate as wildly as primary insurance, the “peace of mind” value is higher here.

- California: Tight regulations on “add-on” products at dealerships mean you might find more transparent pricing here.

- New York: Insurance companies are heavily scrutinized, often leading to lower add-on costs for gap coverage compared to other states.

9. How to Cancel Gap Insurance and Get a Refund

One of the best-kept secrets in the industry is that gap insurance is often refundable. If you sell your car, trade it in, or pay off the loan early, you are entitled to a pro-rated refund of the “unused” portion of your gap policy (if you bought it from a dealer).

The Process:

- Find your original contract: Look for the “Gap Waiver” or “Gap Insurance” document.

- Contact the administrator: This is usually a third-party company, not the dealership itself.

- Provide proof of payoff/sale: A letter from your bank or a bill of sale will suffice.

- Follow up: Don’t expect them to send the check automatically. You have to ask for it.

10. Common Myths About Gap Insurance Costs

Myth 1: “Gap insurance covers my engine if it blows up.”

Reality: No. That is a Mechanical Replacement or Extended Warranty. Gap only triggers if the car is a total loss (accident or theft).

Myth 2: “I have ‘New Car Replacement’ coverage, so I don’t need Gap.”

Reality: These are similar but different. New Car Replacement gives you a brand-new version of your car. Gap just pays off the bank. Sometimes you need one, sometimes the other, but rarely both.

Myth 3: “Gap insurance is required by law.”

Reality: No state law requires gap insurance. However, your lender or leasing company may require it as a condition of the contract.

11. Top 5 Tips to Save on Gap Insurance

- Shop Around Before Going to the Dealer: Call your insurance agent before you go to the car lot. Get a quote for gap coverage so you have a baseline.

- Negotiate at the Dealership: If you must buy from the dealer, negotiate the price. They can often drop the price by 30-50% if they think you’ll walk away from the deal.

- Check Your Credit Union: If you are financing through a credit union, they often offer gap insurance for a flat $200-$300, which is a great middle ground.

- Monitor Your Equity: Once your car is worth more than the loan, cancel the policy immediately. There is no point in paying for coverage that will never pay out.

- Avoid Financing the Premium: If you buy a standalone policy or dealer policy, pay for it in cash upfront rather than rolling it into the loan to avoid interest.

12. Advanced Strategies: The “LTI” (Loan to Insurance) Synchronization

To truly master your finances, you should treat gap insurance as a diminishing necessity. Use free tools like Kelley Blue Book or Edmunds to track your car’s value every six months. Compare that to your bank statement showing your remaining loan balance.

The moment those two lines cross—where the value of the car is higher than the loan—you have achieved “Positive Equity.” At this exact moment, your gap insurance becomes a “phantom expense.” It provides $0 in benefit because there is no “gap” to cover.

Pro Tip: Set a calendar reminder to check this every six months. Spending 5 minutes to check could save you $60 a year in unnecessary premiums.

13. Understanding the “Fine Print” (Exclusions)

Not all gap policies are created equal. Even if the cost is low, you need to check for these common exclusions:

- The 125% Rule: Some policies only cover up to 125% of the car’s ACV. If your gap is massive (e.g., you rolled over a huge amount of negative equity), you might still owe money.

- Past Due Payments: Gap insurance will not cover late fees or missed payments you owed the bank before the accident.

- Commercial Use: If you are using your car for Uber or DoorDash, a standard gap policy might be voided unless you have a commercial endorsement.

14. What Happens During a Claim?

If the worst happens and your car is totaled, here is how the money flows:

- Your primary insurance determines the car’s value (e.g., $20,000).

- They send that $20,000 (minus your deductible) to your lender.

- Your lender says, “Wait, you still owe us $25,000.”

- You file a claim with your Gap Insurance provider.

- The Gap provider verifies the math and sends the remaining $5,000 (and sometimes your deductible) to the lender.

- Your loan is cleared, and you can start fresh with a new car.

Without this coverage, that $5,000 would be an anchor around your neck while you try to finance your next vehicle.

15. The Impact of Inflation on Gap Insurance

In recent years, the used car market in the US has been volatile. When used car prices skyrocketed, many people suddenly found themselves with positive equity, rendering their gap insurance temporarily useless. However, as prices normalize and car values drop, the “gap” is returning with a vengeance.

Paying for gap insurance in a volatile market is a hedge against a sudden “market correction” where your car’s value could drop by 20% in a single month.

Advice from xyzhelp.com

At xyzhelp.com, we’ve seen thousands of consumers struggle with the hidden costs of vehicle ownership. Our professional advice regarding gap insurance is simple but firm:

Do not buy gap insurance at the dealership unless you have no other choice. The markup is simply too high. Before you even step foot on a car lot, call your current auto insurance provider. Ask them for a quote on “Loan/Lease Payoff Coverage.” If they offer it for under $100 a year, take it. If they don’t offer it, check with your bank or credit union.

Only use the dealership’s gap insurance as a last resort, and if you do, negotiate the price like your life depends on it. Remember, gap insurance is a financial tool, not a dealership donation. Protect your wallet as much as you protect your car.

Final Checklist from xyzhelp.com:

- Check if your lease already includes it.

- Compare dealer vs. insurance company rates.

- Check for a “deductible reimbursement” feature.

- Cancel the policy once you have positive equity.

- Always read the “Exclusions” section of the contract.

Safe driving and smart spending!

Disclaimer: This guide is for informational purposes only. Insurance rates and regulations vary by state and individual circumstances. Always consult with a licensed insurance professional before making financial decisions.